In 2012, we have seen risk management and sustainability play a more important part in the agendas of leading fashion brands. Nevertheless, many companies still perform poorly at many stages of their supply chain and are unaware of the risks, particularly if they lie beyond their direct operations.

The following are the the main trends we see happening in the near and mid future. A few exist already but will become substantially more pronounced; others are just about to emerge and hit the surface of public awareness.

After 10 years in the make, CETI, the European Centre for Innovative Textiles, was finally inaugurated in October 2012. The aim of the research centre is to give the textile industry a platform to research and prototype innovative textiles that can be used in sectors like: Medical, Sport & Leisure, Hygiene, and Protection sectors representing 25% of technical textile manufacturing industry; building and civil engineering that account for 10% of the production; transport making 26% of the market volume (and 15% of the market value) of technical textiles.

In the discussions within companies around risk management and indispensable moves towards more sustainable processes and business practises, there’s habitually unmentioned elephant in the room, namely: Where, in all what needs to be done in the corporate world, does the responsibility of the individual factor in?

“Show me there is demand, and we’ll be happy to cater to it.” is the most frequently received answer when asking CEOs of consumer goods companies, fashion and apparel in particular, as to why they are not producing better, more sustainable (ecological and ethical) products.

This new report, combines – to the best of our knowledge – all available data about the increasingly popular consumer demand for more responsible products in EU countries.

If there is an area of fashion that is truly pushing the boundaries of what is technically and style-wise possible, then it is Haut Couture.

In January 2013 2 pieces among Iris van Harpenr’s 11-piece collection at Voltage show attracted the interested of fashionistas as much as product techies: The first ever wearable dresses created through a 3D printing process.

2045: scenarios for the textile and fashion industry: How will the industry look like in 5, 10 and 30 years time? Scenarios offer research-based insights, and potentially can show how realistic a world is, that looks rather quite different from what we're used to. What if Asia become today's Europe? What if we did not buy to own? What if everyone was a maker?

China is the set to be the next big consumer market. Brands and retailers – hoping in this way for a few more loops of ongoing growth without reconsidering their business model – are scrambling to get their foot down in the country. The most exclusive retail addresses in Shanghai, Bejing, Hong Kong and many other metropolitan areas sell out in record time and at record prices.

In the fashion industry we’re very taken to ‘trend’: the colours, cuts, styles, fabrics of the next couple of seasons or so. Yet few venture to think about how their very own industry will look like in, say, 2020 or beyond. Resting the case for the importance of building scenarios of the long-term future.

The fashion industry, nearly like no other, has gone through dramatic changes in the last 20, 30 years. Indeed it finds itself in the present at a crossroad. Resource scarcity is triggering shifts in business models and supply-chains; waste is the new resource; customers are the sales channel of the future; and legislation is becoming ever more stringent. The fact though is: if looking back at predictions of the 1950 and 1960, or even earlier (physical artefacts not considered), the reality we live in compares best to the predictions that were considered ‘totally crazy’ in their time.

On November 12 and 13, 2013 the yearly Textile Exchange conference took place in Istanbul, Turkey.

I was invited to run a workshop on Scenario Work as one of the 'Strategy' break out session on the first day. The workshop was fully booked with 25 highly interested and active participants. In 90 challenging minutes they experienced a compressed version of a Scenario Planning workshop.

n early April this year we released a report that consolidated 60 studies, from the time period 2005 to early 2013, on the behaviour, attitudes, shopping criteria of the ‘better consumer’. Over the summer, two of the source reports used for our evaluation have been updated, expanded and released in their 2013 edition with further relevant details.

Supply chains, as a discipline of expertise, have come out of the hiding and recognise their role in reducing corporate risk. This is notably and specifically the case in fashion and textiles. At the same time, 'design' - not just in the creation room, but in all facets where it impacts the making, delivery and use of a product or service, is increasingly recognised as relevant.

At Shirahime, we have worked quite extensively over the last few months on the development of fashion industry scenarios beyond the 2020 time frame, going as far as 2045.

We mentioned for example Shell as one that used this approach to suit their own goals.

Siemens' 'Future Life' video, as presented the The Crystal in London.

A much more interesting approach, and very insightful in terms of methodology, but also how tangible the results are presented, is Siemens’ work on Future Cities

As part of a workshop given at the Textile Exchange 2013 conference, we ran a small survey among workshop participants in order to find out more about their perception of and experience with Scenario Planning. Here the survey results.

We all can see it happening before our eyes: Despite the Paris Climate Agreement to a climate trajectory of ‘well bellow’ 2 degrees (hence where the 1.5C number stems from) – the trajectory is not anywhere near that number. The Inevitable Policy Response (IPR) is the response by governments and legislators around the globe in taking action – hence enacting laws – in line with the 1.5 Degree climate goals.

What would the Inevitable Policy response mean for the consumer goods industries? What could the effects be? This instalment of a 3-part series looks at shifts in costing paradigms, in transportation, and in supply chain structures.

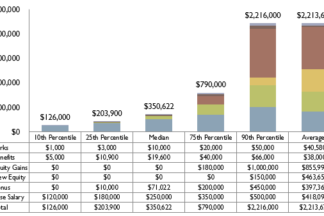

CEO pay is an ongoing topic. Stock options are a regular part of their pay package.

The way CEO pay packages handle stock options may foster short-termism. Or contribute to remedy it. Some thoughts.

What would the Inevitable Policy response mean for the consumer goods industries? What could the effects be? This instalment of a 3-part series looks at: consumption patterns, role of consumer goods industries for economic development, population behaviours when affected by severe conditions

It is end of March / early April 2020 as I write this. Corona (Covid19) increases its grip onto the world. Draconian, tough policy measures are being put in place limiting people's lives ... and rattling the global economy.

Could it hall happen again in the future? And if so - in what way?

When will Corona 'be over'? never. There are historical moments when the future changes direction. We call them bifurcations. Or deep crises. These times are now. Matthias Horx discusses what that means concretely.