In two previous articles, I first reviewed a Bloomberg article that showed how the largest banks by and large are still very biased towards non-renewable energies – largely consequence of the Board of Director’s track record with and in large-scale emitters. In the second article I then looked at precisely those banks and their investment into fossil fuels, coal – as well as their (authentic or not) commitment to phasing these out.

The learnings of the above articles were clear:

- Board of Directors – non-executive as well as executive boards – are fundamental in pivoting banks use of their money towards a trajectory suitable to the energy transition.

- Further, the carbon footprint contribution by means of use of the bank’s cash to a company’s Scope 3 carbon footprint may potentially be rather quite significant.

The consequential logic of these arguments is evident: If companies of all industries are deeply looking into decarbonising their value chain, they will have to look deeply also under the hood of their banking partner/s – and very likely have highly embarrassing (for the banking partner) conversations with them.

Interestingly: For many companies, their total greenhouse gas emissions would be significantly higher if emissions from cash holdings in the bank were counted – because of how the bank would invest them. It is for many a company sheer luck that these emissions are currently not quantified or reported in corporates’ greenhouse gas accounting.

Which of course does not make them less relevant or substantial when looking at the bigger picture of our global carbon trajectory.

And not only that: what applies to the global carbon budget would, and indeed does, apply to the resource availability, biodiversity, human rights (and their abuses) etc. In fact, these ‘extended Scope 3’ impacts of the money in a bank are very real, very relevant – and often very much flying under the radar.

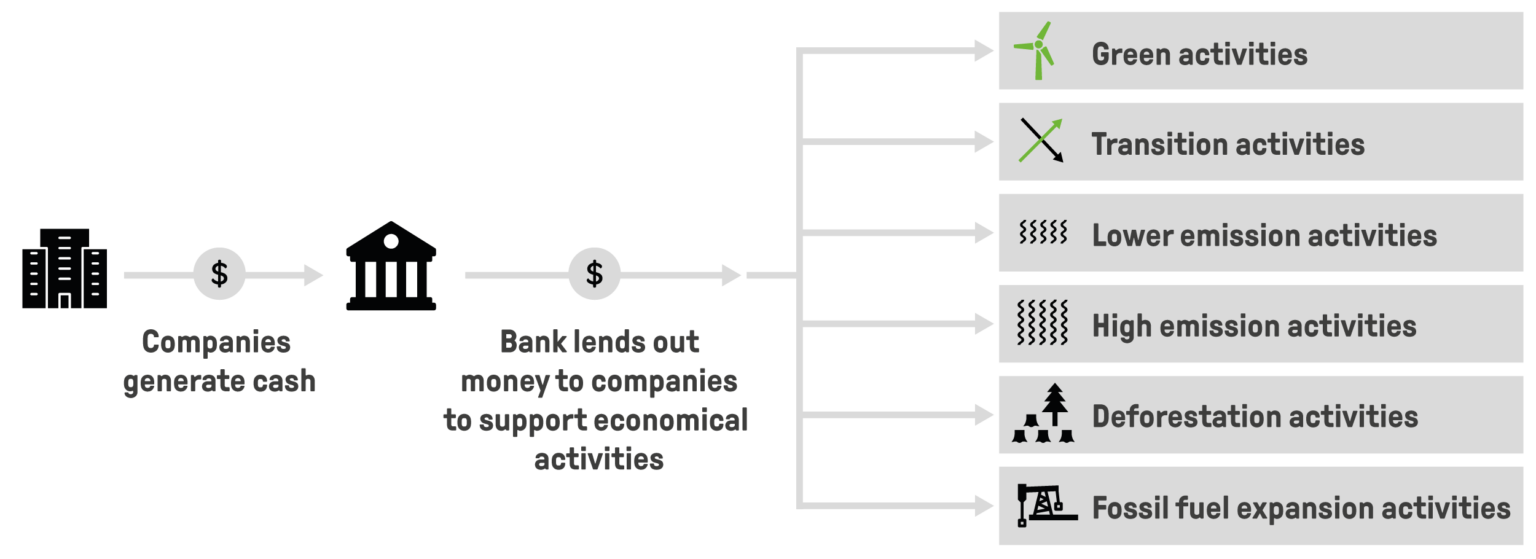

Hold on: What are we talking about??? – The financial supply chain

Every organisation has a financial supply chain similar to its material supply chain. The financial supply chain includes suppliers of financial services such as cash management, pension scheme managers, asset lease partners and so on. Just as the material supply chain, the financial supply chain also generates emissions. These arise from how financial institutions – in the case of cash: banks – use an individuals or a company’s money to finance activities that generate emissions.

Look at the following two images to better understand what the above admittedly somewhat complicated wording means:

For a company hence, that is neither a bank, nor active in the extractive or fossil fuel / energy business, the question hence immediately is: What can I do about it, and in what way?

The Green Action Cash Guide: Removing financed emissions from Scope 3

Luckily there is many a company that has exactly that very problem. And equally luckily the Exponential Road Map Initiative has realised that challenge, and issues a first – possibly to be refined in the future – guidance document on how to address in first instance this conundrum.

What follows hereafter is a quick look into and review of the resulting ‘Green Action cash Guide’.

Side note: the beauty of this guide is that while written for companies, and specifically with a view also to SMEs, even the retail consumer client – each of us individually – can use the same approach to talk to their house bank. That again is great news, and indeed a 2-flies-with-one-stone strike!

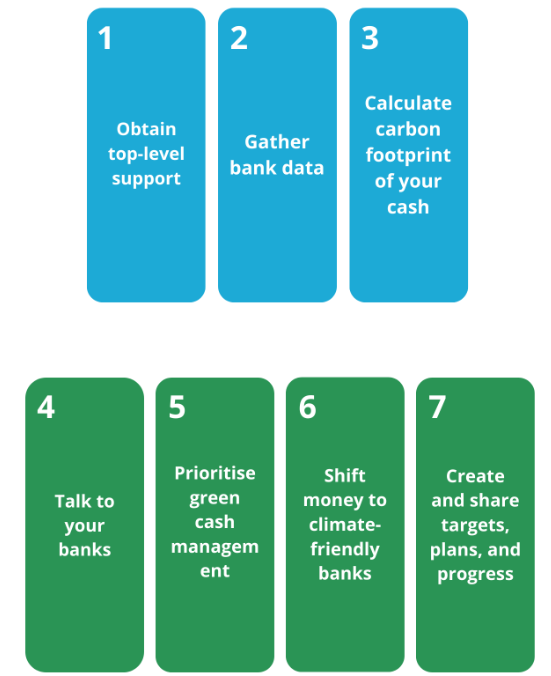

The Guide outlines 7 concrete action steps to address the issue (cf. Figure 3):

How valuable and ‘matter of fact’ are the details provided by the guide for each of the action steps? Let’s have a more detailed look.

- Obtain top-level support

- Relevance: As a concept, this one is of course straight forward, because you can expect that such a fundamental issue will sooner or later land with your CFO.

- Tangible support provided in the guide: Not much. It comes down to the fact that either senior management ‘sees the point’ and understand the bigger picture … or not. Period. I’d have liked to see deeper going material also referring to e.g. stock exchange regulation (US SEC to take on example), institutional investors’ strategies, and board’s duty of care.

- Gather Bank Data

- Relevance: What you can’t measure, you can’t manage. So this is again a valid and well made point.

- Tangible support provided in the guide: Page 7 of the guide does offer check list with 3rd party resources that come in handy to gather and evaluate the data. It’s not perfect, and is missing the ‘Banking on Climate Chaos’ yearly updated ‘Fossil Fuel Finance Report’.

- Calculate Carbon Footprint of your Cash

- Relevance: This is actually part 2 of the above 2nd point, and therefore a fundamental step to get a clear(er) idea and at least an estimated baseline.

- Tangible support provided in the guide: Half-way useful. The formulate given to estimate the banking partner’s carbon emissions (Value of Cash Deposits x Carbon intensity of the bank’s lending = Emissions of cash holdings) is helpful IF the bank publishes their carbon intensity. Which tough most of the banks do not do.

It would have hence been useful to get another piece of guidance on how to get at least to a very basic ballpark figure if the bank does not publish their carbon emissions ….

- Talk to your bank

- Relevance: Evidently high assuming you’re serious to rattle the bank’s boat a bit.

- Tangible support provided in the guide: Decent, if not perfect. There is a question list and some advice.

However, it would have been useful to add a list of warning flags in the responses to look out for, notably those linked to potential green-washing, and how to follow up on these areas if deemed useful / necessary. In other words: what’s absent is a piece of guidance on how to assess the bank’s responses, and how to react to them.

- Prioritise green cash management

- Relevance: High, because evidently that’s part of the decarbonisation efforts of your company

- Tangible support provided in the guide: Very little. The one operational advice that is worth its salt is the following: ‘Asking for your company’s cash holdings to be kept separate from fossil fuel investments’

- Shift money to climate-friendly banks

- Relevance: High given the context, albeit we can have discussion if this is not the same challenge that lies with the ‘de-investment’ strategy of investors: if you’re not invested you have no word, and less scrupulous people will happily take over your share. But at least the prospect of losing a client may certainly be a an issue for a bank. And there is no doubt that we need a lot more and better ethical banks that get to a size that allows them to offer top market rates for most products also.

- Tangible support provided in the guide: The guidance is pragmatic and goal driven, hence well done in principle. What is missing here: a list by country of banks – small and large – that would be suitable to run corporate accounts (and if so, how large such accounts could / should be …)

- Create and share target plans, and progress

- Relevance: This seems to be a bit boiler plate – if you have a climate / sustainability strategy then this is obviously part of the game.

- Tangible support provided in the guide: Not particularly useful, very generic, and could by and large be written into any guidance of any type of action. I missed in particular the regular follow with the bank on their trajectory, as well as the communication to the bank what their carbon footprint meant for your own banking strategy …i.e. giving them timelines on how they might be phased out if their footprint is not moving sufficiently.

Very helpful though overall is the link to the efforts made by ‘The Carbon Bankroll’ project and report, and particularly to the template and questionnaire repository they offer.

Conclusion

This is a decently done guide, that though is kept at a fairly high level, and misses some depth in the support section, i.e. ‘the ‘how to do it concretely’ aspect.

There are several ways of how that could be addressed:

- Case studies for each steps outlining how it had been done, the hurdles encountered, the insights and learnings gained.

In other words: each section misses a ‘how to do it hands on’ subchapter. - Link each section to template/s, calculators etc that help getting the job done. Likely they will exist already, but making the specific template/s etc a firm part of the step to be taken would take mental load of those poor corporate finance individuals who have to deal with the banks directly.

- Latest when the conversations comes to switching banks, the resources on where to find such banks – those lists exist from 3rd parties – might have been handy. Rather than to include them in the annex …

It also happens that the mentioned list does NOT provide insights for many Global North markets … which is a fundamental issue. Also here I wonder if there would not have been some means or resource to close that gap. - Some additional guidance for micro-enterprises, as well as M-sized multi-nationals would have been a good idea. Both of these encounter very specific challenges that merit some extra support. The first due to the lack of clout – sometimes just being very glad to have a viable banking partner at all – and the second on the hurdles that come with international cash operations across borders …

The added value of the guide – being viable for individuals also – is a nice one and a good surprise. It is largely a consequence though of the lack of depth in some areas. It is a good first edition of the guide, but I would hope that in a year’s time an update follows that closes some of the remaining support gaps and offers more operational hands-on help.